Backtesting Trading Strategies Before You Trade Real Money

Backtesting is the process of testing trading strategies on historical data to evaluate whether a strategy could have generated a profitable trade or series of trades in the past. Instead of immediately risking real capital, a trader can simulate how a strategy would behave under past market conditions.

In modern stock trading, backtesting allows traders and investors to evaluate a trading idea, measure risk, and analyze potential profit or loss before placing a single trade in the live market.

A typical backtest recreates the decision process of a trading system using historical market data. The goal is to determine whether the trading strategy would produce acceptable trading performance, reasonable drawdown, and consistent profitability across various market conditions.

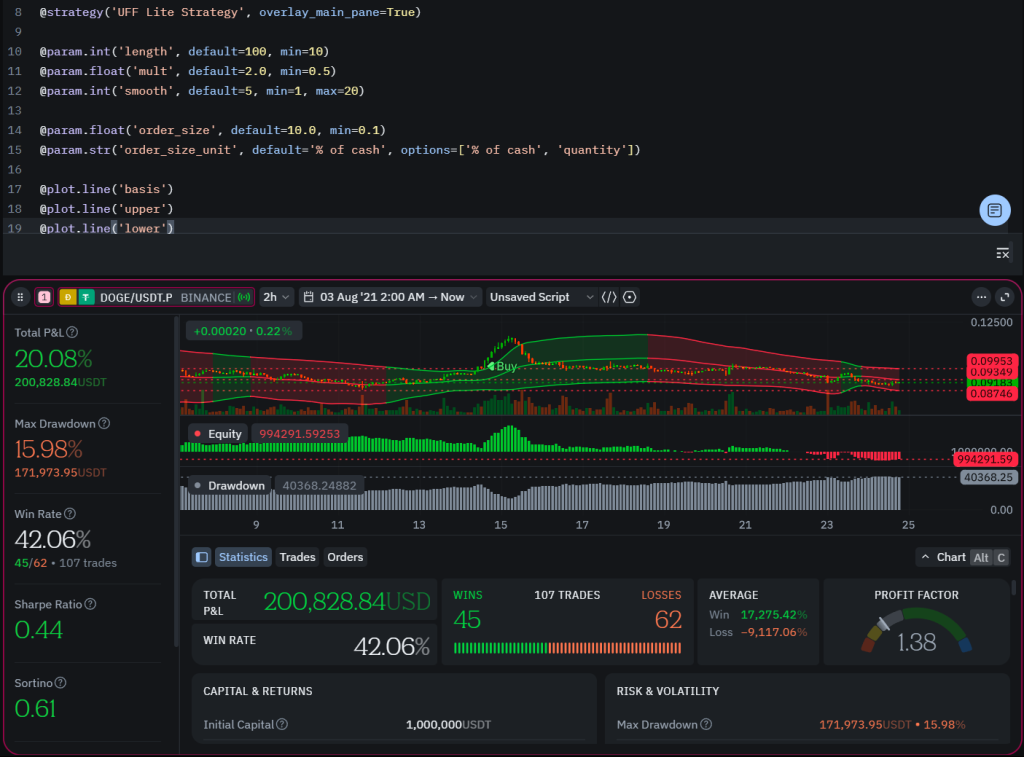

Professional traders often rely on backtesting software such as TradingView or TakeProfit to test your trading ideas and validate the viability of a trading strategy before deploying it with real money.

Backtesting a Trading Strategy to Refine Trading Strategies and Portfolio Risk

Backtesting a trading strategy helps traders understand how their rules behave over long backtesting periods. This process helps identify weaknesses and refine the rules of a strategy before using it in real markets.

When backtesting a strategy, the platform will:

- Apply entry and exit rules to historical data

- Simulate each trade exactly as it would occur

- Track profit and loss for every position

- Calculate metrics like drawdown, volatility, and Sharpe ratio

The Sharpe ratio is a measure often used in finance as a measure of risk-adjusted return, helping traders understand whether a strategy’s returns justify the level of risk taken.

By repeatedly running backtesting, traders can refine your strategy and improve the overall profitability of their trading strategies.

How Backtesting Uses Historical Data to Backtest a Trading Strategy

The core principle of backtesting is applying a trading strategy to historical market data to determine whether it could have generated profitable trade opportunities.

A basic backtest a trading strategy workflow includes:

1. Define the Trading Rules

A strategy must specify:

- entry and exit signals

- position size

- stop-loss and take-profit

- trading costs

For example, a stock trading strategy might use moving averages, such as a simple moving average crossover.

Example trading idea

- Buy when the 50-day simple moving average crosses above the 200-day average

- Sell when the crossover reverses

This type of strategy is common in both stock and forex strategy development.

2. Apply the Strategy to Historical Data

Using years of data, the system will evaluate every possible trade signal. This simulation allows a trader to see how the strategy performed across bullish and bearish trends.

This process is called automated backtesting, although some traders still prefer manual backtesting.

3. Analyze Backtest Results

Once the system completes the simulation, traders review backtest results and backtesting results, including:

- win rate

- profit and loss

- maximum drawdown

- volatility

- Sharpe ratio

These metrics help determine the viability of a trading strategy and whether it could potentially beat the market.

Manual Backtesting vs Automated Backtesting

There are two main methods of backtesting used by traders.

Manual Backtesting

With manual backtesting, a trader scrolls through charts and records each trade manually.

This method helps traders learn market structure and develop intuition. Some traders even manually backtest a strategy using chart replay tools.

However, manual analysis can be slow and may introduce human bias.

Automated Backtesting

Automated backtesting uses trading software to automatically run a strategy across large datasets.

This method allows traders to:

- test thousands of trade scenarios

- analyze large stock datasets

- run scenario analysis

- measure risk across a portfolio

Automated tools are now the best backtesting approach for most algorithmic traders.

Using TradingView for Backtesting and Replay Analysis

Many traders perform backtesting using TradingView because it provides powerful charting and scripting tools.

When using TradingView, traders can:

- write strategy scripts

- simulate trades automatically

- use replay mode to review past market behavior

- analyze backtesting results

TradingView is widely used by both beginners and professional traders for strategy testing, paper trading, and developing new trading strategies.

Other platforms such as TakeProfit offer additional backtesting tools, screeners, and custom scripting languages designed for advanced trading software workflows.

Backtesting vs Paper Trading in the Live Market

A common comparison is backtesting vs paper trading.

Backtesting

- uses historical data

- evaluates hypothetical trades

- allows risk-free testing

Paper trading

- occurs in the live market

- uses simulated funds

- reflects real-time market environment

Many traders follow this workflow:

- Started backtesting a trading strategy

- Validate the backtesting results

- Test with paper trading

- Deploy the system with small capital

This approach allows traders to test ideas without risking real capital.

Portfolio Backtesting and Scenario Analysis

Advanced traders often run portfolio tests instead of analyzing a single stock.

Portfolio backtesting measures how multiple trading strategies behave together.

This allows traders to:

- evaluate diversification

- reduce overall risk

- perform scenario analysis

- test performance in different market environments

Sophisticated systems also use in-sample and out-of-sample data to verify that strategies do not produce artificially high returns due to overfitting.

Common Backtesting Pitfall Traders Should Avoid

Even experienced traders can make mistakes when performing backtesting.

A common pitfall is overfitting, where the strategy is optimized too heavily for past data.

This can lead to systems that look perfect historically but fail in the live market.

Other mistakes include:

- ignoring trading costs

- using incomplete historical data

- testing only surviving stock companies while ignoring those that went bankrupt

Professional backtest should consider realistic conditions including spreads, fees, and slippage.

Why Backtesting Matters for Traders and Investors

For traders and investors, backtesting plays a crucial role in finding a strategy that works consistently.

A properly backtested strategy helps:

- improve trading decisions

- measure potential risk

- understand strategy profitability

- prepare traders for changing market conditions

Instead of guessing or relying on intuition, traders can test your trading ideas using data.

This approach ensures that trading strategies without proper validation are not used with real money.

Conclusion

Backtesting is a fundamental process in modern trading methods. By applying trading strategies to historical data, traders can evaluate the potential profit or loss of a strategy before deploying it in the live market.

Whether you are testing a stock strategy, a forex trading strategy, or a diversified portfolio, the goal of backtesting is always the same: validate the strategy, measure risk, and improve trading performance.

When combined with paper trading and proper scenario analysis, backtesting becomes one of the most powerful tools for developing profitable and robust trading strategies.

Leave a Reply